1800-270-7000

1800-270-7000

Retail NPS made simple

Think of this as your own retirement plan.

Retail NPS is designed for individuals who want to invest for their future — independently.

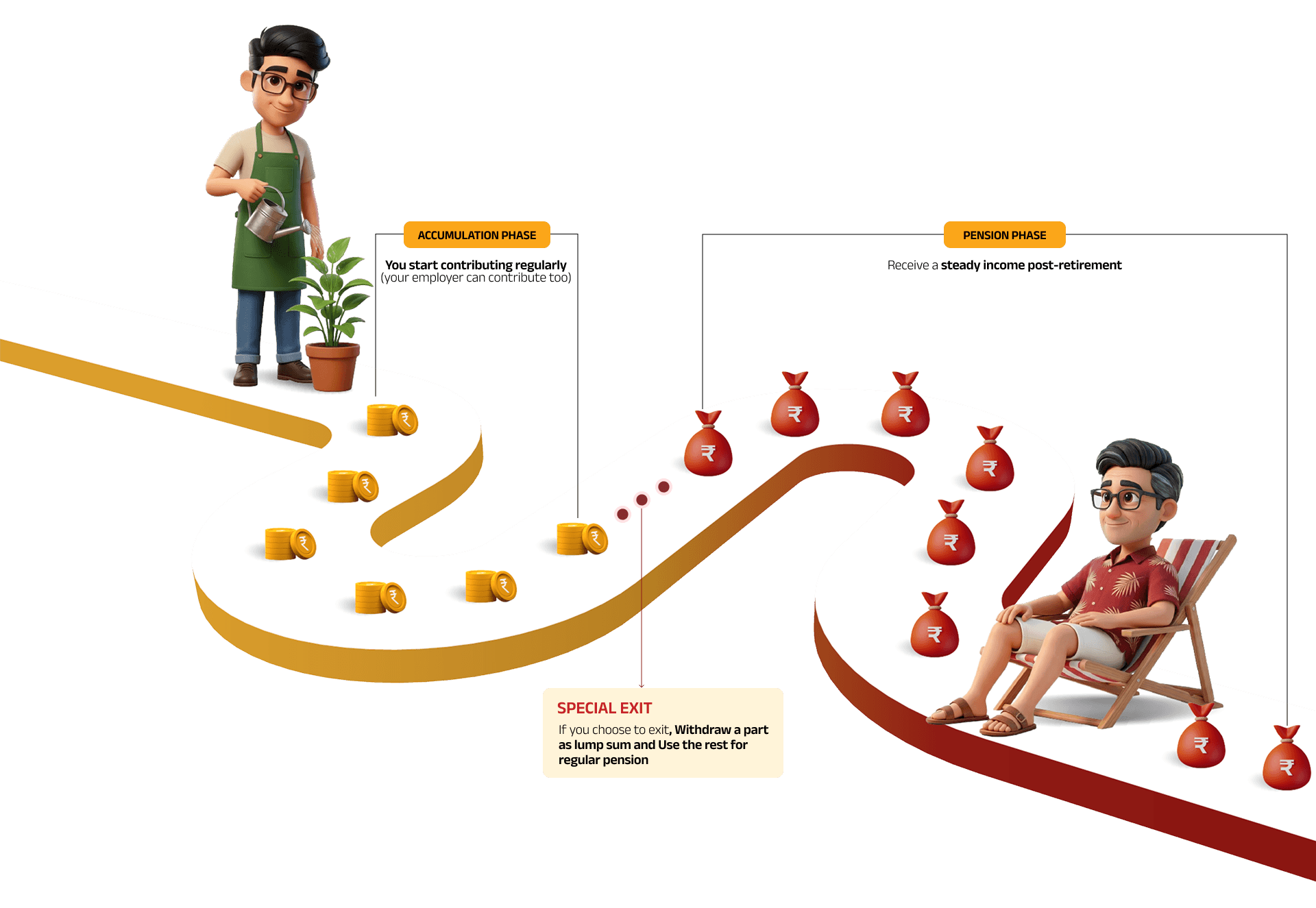

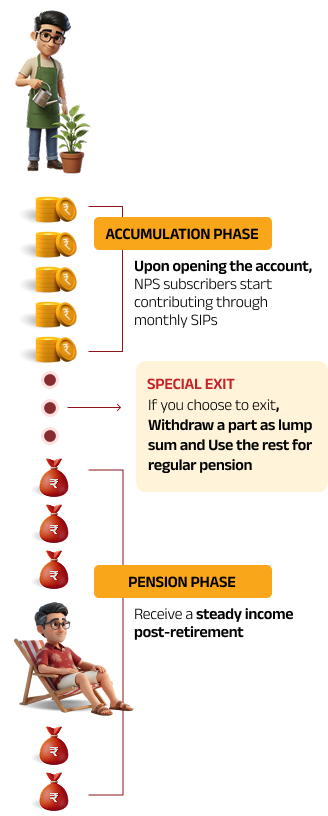

You contribute regularly. Your money is invested across equity and debt.

Over time, this builds a retirement corpus that supports you with income later.

All within a regulated, low-cost framework under PFRDA.

If you’re | you are eligible!

Unlock additional tax savings with Retail NPS, a tax efficient pension scheme, under 80CCD(1) and 80CCD(1B) available in old tax regime

Over 1.65 crore Indians are already building their future with Retail NPSSource: Press release 22nd April 2025, Ministry of Finance, www.pib.gov.in

Start your own retirement plan

No employer required — you’re in controlSave more on taxes

Up to ₹2 lakh in deductions under Sections 80CCD(1) & 80CCD(1B)Built for long-term growth

Market-linked investments that compound over timeFlexible and portable

Change jobs, cities, even goals — your account staysLow-cost investing

More of your money stays investedStay invested. Watch it multiply

Make your next innings count

Opening your Retail NPS online is quick and straightforward.

Go to the ‘Contribute’ section

Start your NPS journey online

Enter your details

Fill in your basic information

Verify your PRAN

Confirm your account details

Make your contribution

Complete your payment securely

Watch. Learn.Get Started. See the process in action

Prefer to do this offline?

If you’d rather do this in person, you can visit our nearest branch and get started easily.

Visit a branch

Head to your nearest Point of Presence (PoP)

Fill in your details

Complete the registration and KYC forms

Receive your PRAN

Your account is processed by CRA (Central Record Keeping Agency) and your PRAN details are shared.

Make your first contribution

Deposit your cheque along with the NCI slip (NPS contribution instruction slip) at the PoP.